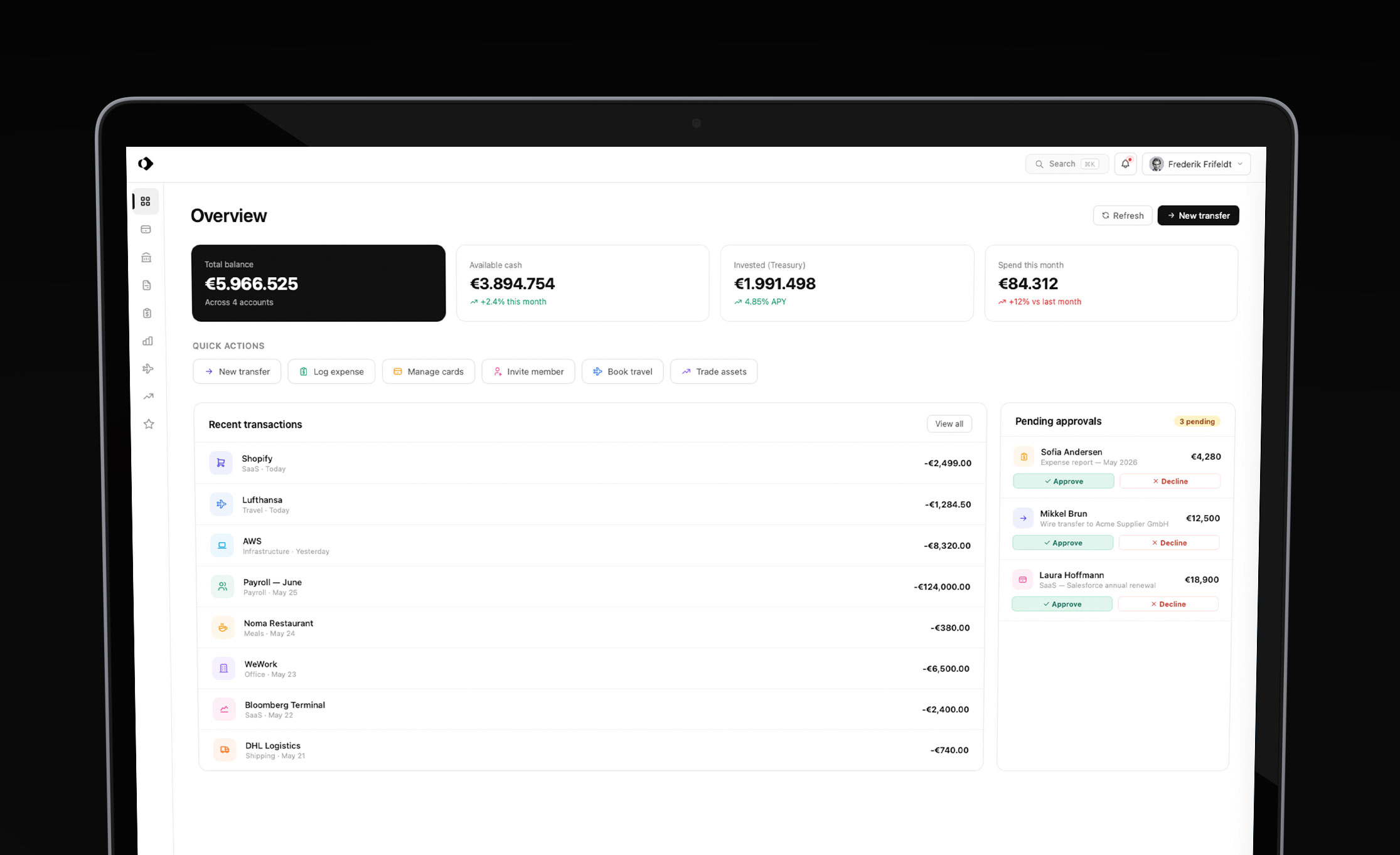

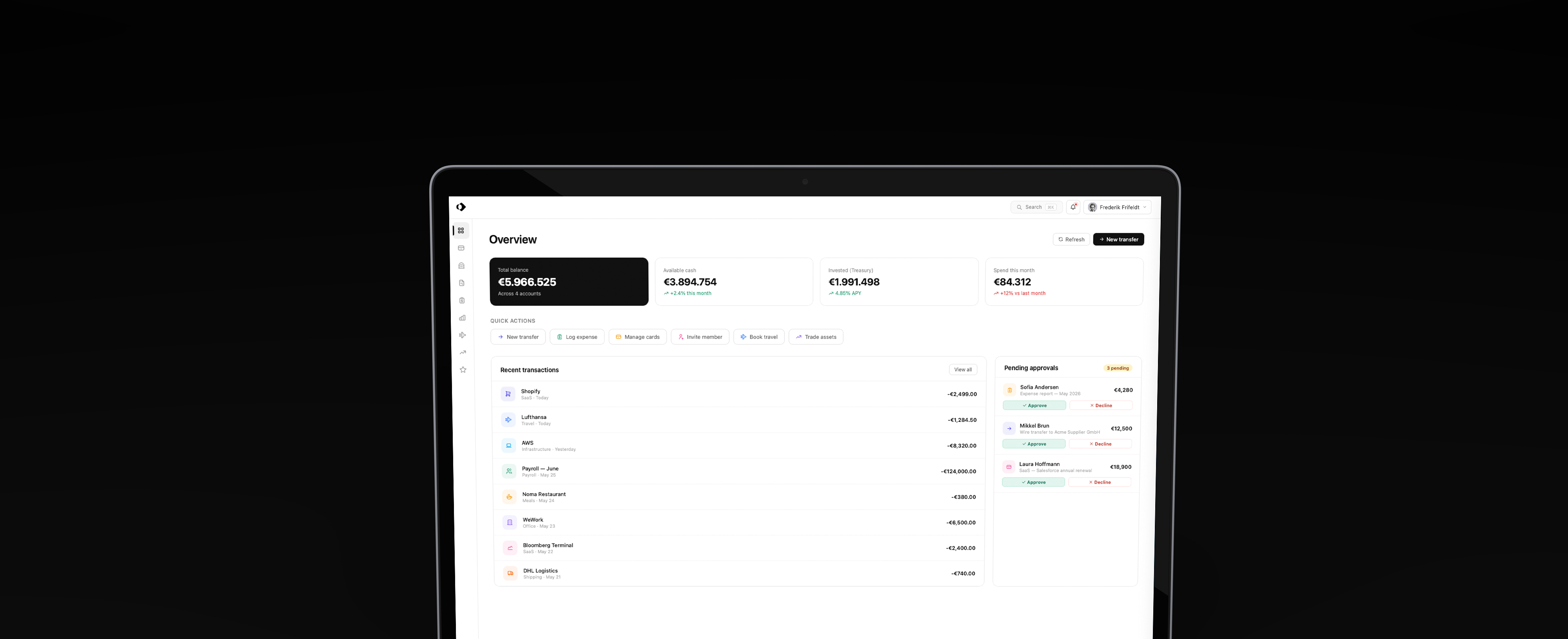

The corporate card European businesses actually want.

Visa cards with up to 50% cashback on business products, built-in travel booking, and bookkeeping that automates itself — all in one account. Ready in minutes, not months.

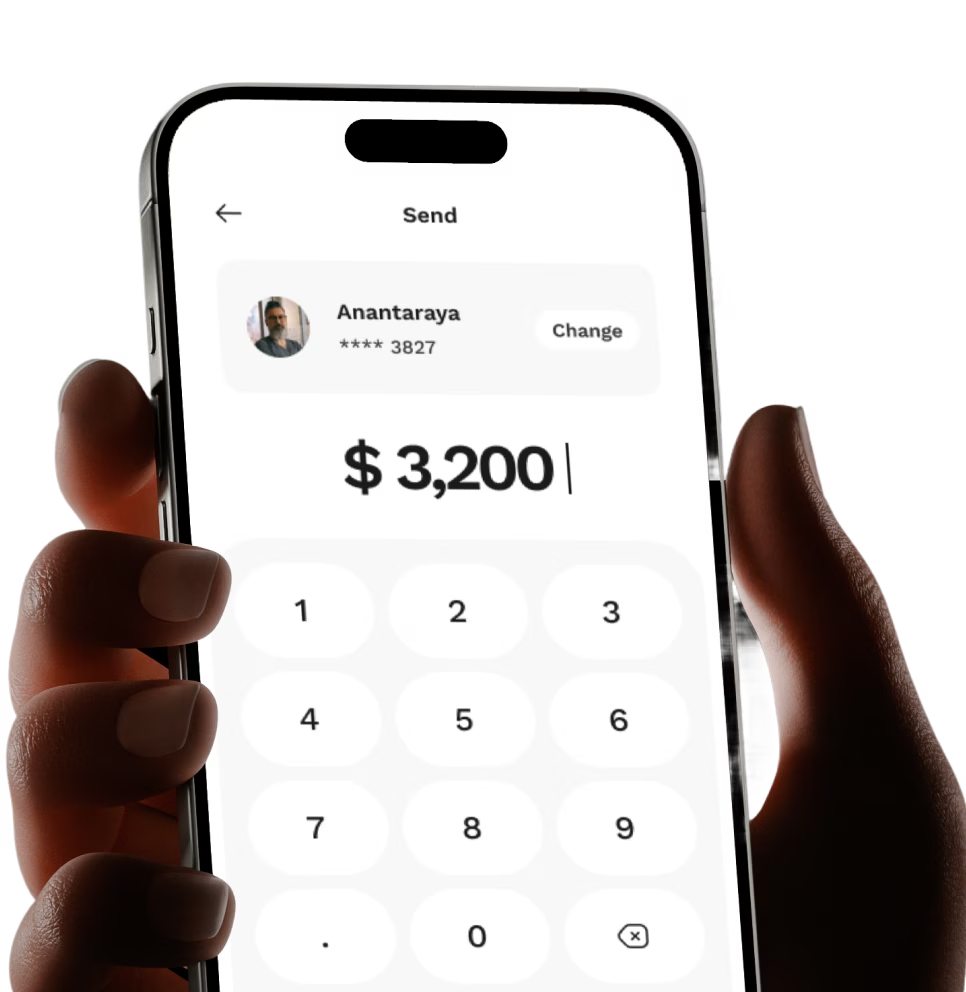

Book flights and hotels right inside Eduvo. Every trip is charged to your company card, earns cashback, and lands in your books automatically — no reimbursements, no lost receipts.

From startups to enterprise — real results from real teams.

Sarah Lee@slee_designs

"Eduvo has transformed our workflow. The integration was seamless and our productivity has soared!"

Daniel Cho@dancho_fin

"Switching to Eduvo was the best decision for our finance team. Payouts are faster, reporting is clear."

Michael Turner@mturner_dev

"After using Eduvo, I can't imagine going back. The user interface is intuitive and customer support is top-notch!"

Emily Chen@echen_marketing

"Since adopting Eduvo, our finance process has streamlined significantly. Cards and expenses all in one place."

Jonathan Smith@jsmith_sales

"Eduvo's analytics help us make data-driven decisions effortlessly. Monthly close went from days to hours."

Sarah Lee@slee_designs

"Eduvo has transformed our workflow. The integration was seamless and our productivity has soared!"

Daniel Cho@dancho_fin

"Switching to Eduvo was the best decision for our finance team. Payouts are faster, reporting is clear."

Michael Turner@mturner_dev

"After using Eduvo, I can't imagine going back. The user interface is intuitive and customer support is top-notch!"

Emily Chen@echen_marketing

"Since adopting Eduvo, our finance process has streamlined significantly. Cards and expenses all in one place."

Jonathan Smith@jsmith_sales

"Eduvo's analytics help us make data-driven decisions effortlessly. Monthly close went from days to hours."

FAQ

Frequently asked questions

Everything you need to know about using Eduvo.

How quickly can I start using Eduvo?

+

Complete KYC in minutes and issue virtual Visa cards immediately — no branch visit required.

Which countries are supported?

+

Eduvo is live in Spain, United Kingdom, Denmark, Sweden, and Norway, with more European markets coming soon.

How does cashback work?

+

You earn 0.5% cashback on all card spend, and up to 50% cashback on business products — software, SaaS, and services bought through Eduvo partners. Cashback is credited to your balance monthly.

Is Eduvo regulated?

+

Yes. Payment services are provided by our partner, a Payment Institution authorized by the Finantsinspektsioon (Estonian Financial Supervision and Resolution Authority) and an official Visa Principal Member (registration code 11812882), operating across the EEA and UK. PCI-DSS Level 1, PSD2 and GDPR compliant.

Are my funds safe?

+

Your funds are safeguarded by our partner in segregated accounts in accordance with EMI regulatory requirements.

Is there a mobile app?

+

Yes, available on iOS and Android with Apple Pay and Google Pay built in.

Corporate card

The corporate card every growing business deserves.

Where higher spending power meets smarter controls — and expense reports do themselves.

Issue as many physical and virtual Visa cards as your team needs — there's no limit and no per-card charge. New cards are ready in seconds from the dashboard or mobile app.

Earn 0.5% cashback on every transaction — and up to 50% cashback on business products. Upgrade to the Metal Visa Infinite on Scale and get complimentary access to 1,300+ airport lounges worldwide for you and a guest.

Eduvo cards automatically collect receipts, generate memos, and categorise every transaction to the right GL — including across European entities. No chasing employees.

✓ Automated receipt capture on every transaction

✓ AI-powered GL categorisation & memos

✓ Policy enforcement without admin overhead

Spend limits

Customise limits and controls.

Issue spend limits with embedded controls for category, merchant, and amount. Transfer cards in one click — or automatically when an employee leaves.

Earn 0.5% cashback on everything your team spends — and up to 50% cashback on business products. Credited straight to your balance, every month.

50%back

Up to 50% on business products

Earn 0.5% cashback on every euro your team spends — and up to 50% back on business products like software, SaaS, and cloud services through Eduvo partner offers. Everything is credited straight to your balance.

✓ 0.5% cashback on all card spend

✓ Up to 50% back on business products

✓ Credited automatically to your balance

✓ No caps, no expiry

Estimate your cashback

Monthly company card spend

€50,000

€5k€500k

Of which spent on business products (software, SaaS, services)

€10,000

€0€100k

Illustrative only. 0.5% cashback on all card spend; business product cashback depends on partner offers, up to 50%.

How you earn

Flights & hotels

Flights & hotels booked via Eduvo Travel earn cashback too

Account cashback

Cashback credited to your balance every month

Business products

Up to 50% back on software, SaaS, and services from Eduvo partners

Scale

Airport lounges

1,300+ lounges worldwide with Metal Visa Infinite

✦

Metal Visa Infinite — benefits worth over €3,000/year

Upgrade to Scale and get the metal card, unlimited worldwide lounge access for you and a guest, and the same cashback on every transaction.

Get IBAN accounts, treasury, and SEPA/SWIFT payments — all in one solution.

IBAN AccountsTreasuryTransfers

IBAN Accounts

Your European headquarters for money.

Get dedicated IBANs in EUR, USD, GBP, SEK, NOK, DKK, PLN, CZK, HUF, and RON — each with its own account number so counterparties pay you in their local currency, without FX friction.

✓ Dedicated IBAN per currency — EUR, USD, GBP, SEK, NOK, DKK, PLN, CZK, HUF, RON

✓ Full multi-currency dashboard across all 5 markets

Most businesses leave significant cash sitting idle earning nothing. Eduvo's treasury trading tools let you automatically invest excess balances — and access your funds the same day you need them back.

✓ Earn yield on uninvested balances

✓ Same-day liquidity — no lock-in periods

✓ Automated sweeps: set your minimum operating balance

SEPA same-day settlement. SWIFT international reach. Schedule recurring payments for payroll, suppliers, or subscriptions — and let Eduvo handle the execution automatically.

Hold, send, and receive in any of our supported currencies — each with a dedicated IBAN. No currency conversion on local transactions, no separate bank account per country.

✓ Dedicated IBAN issued per currency, same day

✓ Available to businesses across the EEA and UK

✓ SEPA and SWIFT from every account

✓ No FX fees on transactions in the matching currency

Accounts are provided by our partner, a Payment Institution authorized by the Finantsinspektsioon (Estonian Financial Supervision and Resolution Authority) and an official Visa Principal Member (registration code 11812882), operating across the EEA and UK.

🇪🇺EUR

🇬🇧GBP

🇳🇴NOK

🇨🇿CZK

🇷🇴RON

🇪🇺EUR

🇬🇧GBP

🇳🇴NOK

🇨🇿CZK

🇷🇴RON

🇺🇸USD

🇸🇪SEK

🇵🇱PLN

🇭🇺HUF

🇩🇰DKK

🇺🇸USD

🇸🇪SEK

🇵🇱PLN

🇭🇺HUF

🇩🇰DKK

Spend management

The future of spend management.

Manage European spend and close the books in real time — with zero manual expense work for your team.

Configure chains that match your org. Amount thresholds auto-escalate to the right approver — managers approve in seconds from mobile.

Clear policy visibility

Every out-of-policy transaction shows exactly why it flagged, so approvers make decisions with full context — no back-and-forth with employees.

Full audit trail

Every approval, rejection, and override is logged with timestamp and user. Audit-ready at any time without manual record-keeping.

"By making it easier for employees to comply, finance went from the bad cop to the hero."

Daniel Cho

VP Finance, Northwave Digital

Receipts & compliance

Get expense reports on time, automatically.

Eduvo automates document collection so your team can close the books faster — without chasing employees for receipts or manually categorising transactions.

✓ Receipts captured automatically on every card transaction

✓ Expense memos auto-generated and fields intelligently populated

✓ Departments and GL categories automatically assigned

✓ OCR matches receipts in any language or currency

✓ Export-ready reports at any time — CSV, PDF, or direct sync

Budgets

Increase accountability with real-time budgets.

Set top-level budgets across departments and assign them to managers. They provision spend to their teams and track usage in real time — no surprises at month-end.

✓ Department-level budgets with live utilisation tracking

✓ Managers provision spend directly to individuals or teams

✓ Budget alerts before overspend — not after

✓ P&L owners have a real-time view into their spend

"With Eduvo, we have one platform where we can send SEPA payments, manage expenses, and set up cards for our entire team."

Daniel Cho

Head of Finance, Northwave Digital

Save hours with payment automation.

Designed to free your finance team for higher-impact work.

01 — Onboard payees

Add suppliers and payees in seconds.

Enter a payee's details once. Eduvo stores them securely and re-uses them for all future payments — no manual re-entry, no risk of human error.

02 — Schedule transfers

Set payments to run automatically.

Schedule one-off or recurring SEPA and SWIFT transfers. Eduvo processes them on schedule — payroll, rent, subscriptions, and supplier invoices handled without manual action.

03 — Route to approvers

Multi-level approval flows, automated.

Set approval thresholds by amount or payee type. Eduvo routes payment requests to the right approver automatically — no chasing over email.

04 — Pay by card or IBAN

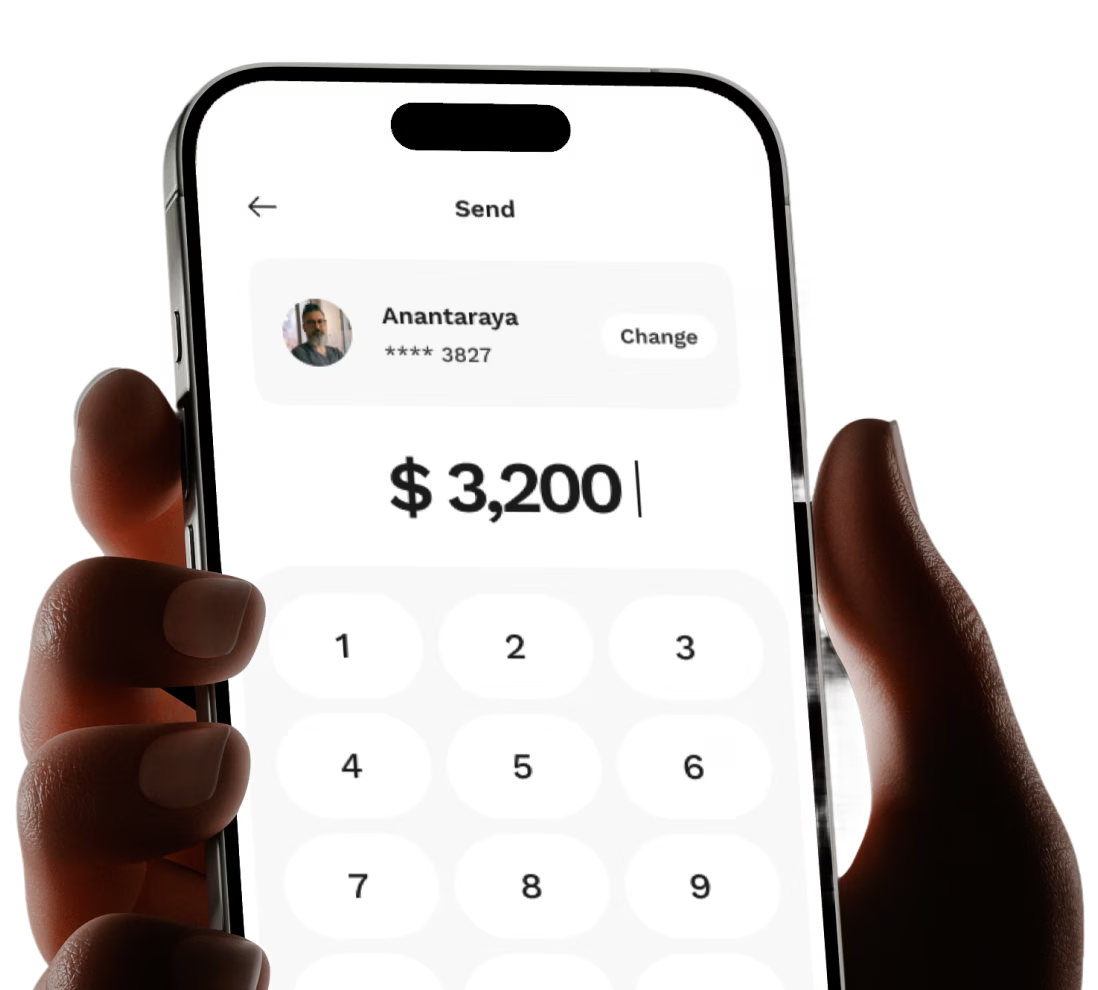

Choose how you pay — earn cashback either way.

Create a virtual Visa card instantly to pay vendors and earn 0.5% cashback. Or send direct from your IBAN via SEPA or SWIFT for maximum speed.

05 — Accept in-store

Visa POS terminals, settled same day.

Take card payments in person with Eduvo POS terminals. Everything settles same day directly into your IBAN — no separate merchant acquirer needed.

Multi-currency payments

Send and receive across Europe — all in one place.

SEPA transfers

Same-day EEA payments.

Send SEPA credit transfers across the EEA with same-day settlement before cut-off. Batch payroll, supplier invoices, and recurring payments — all from one screen.

✓ Same-day settlement before cut-off

✓ Batch payments for payroll & suppliers

✓ Scheduled & recurring automation

SWIFT payments

Global reach in 1–3 days.

Send international payments via SWIFT to banks anywhere in the world. Available across all 5 European markets and in all 5 supported currencies.

Visa POS terminals that connect directly to your IBAN. Contactless, chip & PIN, Apple Pay, Google Pay — settled same day, no separate merchant acquirer.

✓ Contactless, Chip & PIN, NFC wallets

✓ Same-day settlement to IBAN

✓ Unified dashboard with all other payments

"Before Eduvo, we had separate tools for bank transfers, card payments, and payroll. Now having a unified approach to all of this has really streamlined our finance operations."

Jonathan Smith

CFO, Northwave Digital

Manage all your payments in one place.

View all transfers, POS activity, and payment schedules for any period, anytime.

Easy to get started

Eduvo payments are part of your main account — no separate setup, no extra contracts.

Total spend visibility

All payment activity — SEPA, SWIFT, POS, cards — visible in one dashboard in real time.

Earn while you pay

Pay vendors via virtual Visa card and earn 0.5% cashback on every transaction.

Consolidated platform

Payments, cards, IBAN accounts, expenses, and travel — all from one login, one team, one bill.

Travel

Travel management that does the work for you.

Book flights and hotels directly inside Eduvo, auto-enforce travel policies, and unlock worldwide lounge access and travel insurance on Scale — all in one platform.

No one pays us to influence your search results — you see every flight and hotel option at competitive rates.

Control all spend.

Allocate individual travel budgets with custom approval chains. Every booking is visible in real time.

Keep everything compliant.

Pre-enforce spending rules — class of travel, hotel rate caps, advance booking windows. No out-of-policy bookings.

Earn cashback on every trip.

Every booking earns cashback, credited straight to your balance. Scale subscribers also get lounge access and travel insurance built in.

"With Eduvo, our card and spend controls are fully integrated, making it easy for employees to instantly book the business trips they need."

Daniel Cho

VP Finance, Northwave Digital

Manage every trip from booking to expense.

As easy to use as your favourite travel apps — with full spend control built in.

Book directly inside Eduvo.

Search and book flights and hotels straight from the Eduvo dashboard — no third-party booking tools, no switching tabs. Bookings auto-apply your travel policy and spend limits before checkout.

Zero reimbursements.

All bookings charge directly to the company Visa card. No personal expenses, no reimbursement forms, no end-of-trip reconciliation. Everything is in the dashboard the moment it's booked.

Scale

Worldwide lounge access.

Scale plan subscribers get the Metal Visa Infinite card with complimentary access to 1,300+ airport lounges in 140+ countries — for the cardholder and one guest. No per-visit fee, no separate membership.

Scale

Travel insurance included.

Scale plan subscribers are covered by comprehensive travel insurance — including trip cancellation, flight delays, lost baggage, and personal liability. Cover applies automatically on bookings made through Eduvo.

FAQ

Common questions about Eduvo Travel.

Can I book flights and hotels directly inside Eduvo?

+

Yes. Flights and hotels are searchable and bookable directly from your Eduvo dashboard — no third-party booking tool required. All bookings charge straight to your company Visa card and appear instantly in your expense dashboard.

Which plans include lounge access?

+

Lounge access is included on the Scale plan. Scale subscribers receive a Metal Visa Infinite card with complimentary access to 1,300+ airport lounges in 140+ countries via LoungeKey — for the cardholder and one guest, with no per-visit fee.

What does the travel insurance cover?

+

Travel insurance is included on the Scale plan and covers trip cancellation, flight delays, lost or delayed baggage, and personal liability. Cover applies automatically on bookings made through Eduvo — no separate policy to activate.

Do travel bookings earn cashback?

+

Yes. All travel bookings earn the same 0.5% cashback as card spend, credited straight to your balance — and business products booked through Eduvo partners earn up to 50% back.

Which currencies are supported for travel bookings?

+

Eduvo supports bookings in 10 currencies: EUR, USD, GBP, SEK, NOK, DKK, PLN, CZK, HUF, and RON. Your booking is charged straight to your company card in the booking currency — no separate travel wallet to manage.

Is there a mobile app for managing travel?

+

Yes. The Eduvo app is available on iOS and Android. Employees can view bookings, submit receipts with one tap, and managers can approve expenses on the go. Apple Pay and Google Pay are built in for contactless payments while travelling.

Future-proof your travel.

Upgrade your travel and expense programme to the unified platform built for European businesses.

Grow idle balances and eliminate manual cash management — while staying fully in control.

Earn yield

Grow idle cash automatically.

Deploy excess balances into short-term treasury instruments. Set your minimum operating threshold once and Eduvo allocates everything above it — automatically, every day.

Same-day liquidity

Access your funds the same day.

Unlike traditional fixed-term deposits, treasury positions can be unwound same-day. No lock-in periods. No penalties. Your capital is always accessible.

Multi-entity

Manage treasury across entities.

Set allocation rules per IBAN account — EUR, USD, GBP, SEK, NOK, DKK, PLN, CZK, HUF, RON. Treasury is fully integrated with your multi-currency banking dashboard.

Deploy, earn, and access — without lifting a finger.

How it works

Set it once. Let your cash work continuously.

Eduvo treasury setup takes minutes. Define your operating balance threshold and the automation handles everything — allocating, earning, and returning funds as your business needs change.

1

Set your minimum operating balance

Define the floor below which Eduvo never allocates to treasury.

2

Excess cash is automatically allocated

Everything above your threshold sweeps into treasury instruments daily.

3

Yield accrues on allocated balances

Returns are credited automatically — visible in your treasury dashboard in real time.

4

Funds return same-day when needed

When your IBAN balance drops, funds sweep back automatically — no manual action required.

Close the gap between cash sitting and cash growing.

Without treasury

✗ Idle cash earns nothing in current accounts

✗ Manual treasury management takes time

✗ Fixed-term deposits lock funds away

✗ No visibility across multi-currency balances

With Eduvo treasury

✓ Idle balances earn yield automatically

✓ Allocation rules run without manual intervention

✓ Same-day liquidity — unwind any position

✓ Full view across all IBAN accounts in one dashboard

"Eduvo treasury is basically saving us from leaving money on the table every month — it runs completely automatically and we always have same-day access to funds."

Jonathan Smith

CFO, Northwave Digital

Important risk information

Treasury products involve risk. The value of investments can fluctuate and you may receive back less than you invest. Past performance is not a guide to future results. This is not investment advice — seek independent financial advice before making investment decisions.

Eduvo treasury operates within the regulatory framework set by our partner, a Payment Institution authorized by the Finantsinspektsioon (Estonian Financial Supervision and Resolution Authority) and an official Visa Principal Member (registration code 11812882), operating across the EEA and UK. Treasury balances are not covered by FSCS or national deposit guarantee schemes and are subject to our partner's EMI safeguarding rules.

For startups

The financial stack that scales with you.

Get Visa cards with cashback, expense automation, and travel — all in one scalable solution. Ready in minutes, not months.

Every euro your startup spends on Eduvo cards earns 0.5% cashback automatically. Buy software, SaaS, and services through Eduvo partners and earn up to 50% back — credited straight to your balance every month.

✓ 0.5% cashback on all card spend — no caps, no tiers

✓ Up to 50% cashback on business products via Eduvo partners

✓ Cashback credited to your balance automatically every month

✓ PSD2 compliant via our partner — EEA & UK licensed

Card limits tied to your revenue — not a personal credit score. Issue physical and virtual Visa cards to your whole team in minutes, with built-in spend controls from day one.

✓ No personal guarantee required

✓ Unlimited virtual and physical Visa cards

✓ Earn 0.5% cashback on every purchase — up to 50% on business products

"Between the cashback on our software spend and the automated bookkeeping, Eduvo pays for itself every single month."

Daniel Cho

Co-founder & CFO, Northwave Digital

Expense management

Eliminate expense and accounting headaches.

Receipts auto-captured. Memos auto-generated. GL categories auto-set. Your team submits expenses in seconds — your finance team closes the books in days, not weeks.

No more juggling tools. One dashboard for your whole finance team.

Cashback on every euro

0.5% back on all card spend, and up to 50% back on business products — software, SaaS, and services via Eduvo partners.

Smart Visa cards

Issue cards with per-card limits, category controls, and auto-freeze. Physical, virtual, and metal on Scale.

Expense automation

Receipts captured, memos generated, GL coded — all automatically. Real-time reporting across your whole team.

Travel built in

Book flights and hotels in-platform. Earn cashback on every booking, with receipts captured automatically.

Automated bookkeeping

Books that close themselves.

Every transaction lands categorised, with receipt and memo attached, and syncs straight to your accounting tool. Month-end becomes a review — not a data-entry sprint.

✓ GL codes set automatically by merchant-level rules

Set department budgets, assign them to managers, and let Eduvo enforce policy automatically. Real-time spend visibility across teams and subsidiaries — without hiring a finance ops team.

✓ Department budgets with live utilisation tracking

✓ Multi-step approval flows — auto-routed by amount

Gain control and speed across Europe with one card programme for every type of spend, built-in controls, and expense automation that handles the busywork.

No more juggling regional providers, wrestling with FX fees, or drowning in compliance busywork.

Cards

Spend smarter everywhere.

Global Visa card programme with built-in controls. Physical, virtual, and metal cards in one account.

Explore cards →

Cashback

Earn on every entity’s spend.

0.5% cashback on all card spend and up to 50% on business products via Eduvo partners — across every market.

Explore cashback →

Expenses

Eliminate finance busywork.

Automate receipts, approvals, GL coding, and month-end close — across every European entity.

Explore expenses →

Travel

Simplify global travel at scale.

Book, manage, and expense business travel in one platform — with spend limits and policy auto-enforced.

Explore travel →

"The transparency into spend that Eduvo provides is unparalleled. Our finance partners can see exactly how spend is trending at any point in time."

Jonathan Smith

Head of Global Finance, Mintlabs

Automate global financial management.

Eliminate manual work in every spend workflow — from provisioning to approvals to compliance.

Spend controls

Enable and control spend efficiently, locally.

Provision spend limits with built-in policies and issue Visa cards across all 5 markets. Track actuals against planned spend in real time. Automate in-policy approvals to focus on the transactions that matter.

✓ Per-card and per-team spending limits

✓ Merchant category controls & auto-decline rules

✓ Real-time spend visibility across entities

Multi-entity

Easily adapt to foreign markets and regulations.

Customise spend policies per entity, currency, and local tax rules. The right policy applies automatically to expenses — and expense reports are auto-filled to boost compliance across every subsidiary.

✓ Entity-level cards and budgets per market

✓ Local tax & VAT compliance via entity-level mapping

✓ Auto-close across all 5 European markets

Reporting

Make every spend decision a good one.

Real-time reports by entity, team, category, or period — with spend insights the moment a card is swiped, anywhere in Europe.

Spend reports

Spend insights in real time by entity, team, and category — with automatic alerts on anomalous transactions.

Compliance reports

See exactly how much spend is out of policy, which teams are responsible, and track resolution across all entities.

Transaction reports

Filter global card expenses by budget, user, category, or period — exportable to your accounting system at any time.

Security & compliance

Enterprise-grade security, built in.

From PCI-DSS Level 1 card security to PSD2-compliant payment services — Eduvo is built to meet the compliance requirements of large European businesses.

PCI-DSS Level 1

PSD2 Compliant

GDPR & DORA

FSA-licensed partner

3D Secure on all cards

EEA & UK regulated

Implementation

Up and running in days, not months.

Your dedicated account manager guides you through setup. Go live in as little as one week — with priority support throughout.

1

Day 1

Sign up & KYC

Business verification completed online. Virtual Visa cards available the same day.

2

Days 2–4

Configure & set policies

Set up entities, markets, teams, approval workflows, and spend rules with your account manager.

3

Day 5–7

Issue cards & go live

Issue cards to the whole team, onboard your first entities, and go live with full expense management active.

Eduvo for Marketing & Advertising

Finance as smart as your creative.

Great campaigns shouldn't wait for cash flow. Eduvo lets you control client budgets, earn cashback on ad spend, and pay freelancers instantly — across Europe.

Eduvo gives marketers and agencies the confidence to move fast, keep clients happy, and focus on delivering breakthrough work.

Stay profitable on every campaign.

Issue Eduvo Visa cards with spend limits per client or campaign. Auto-enforce policies on every transaction and get real-time alerts before overspend eats into margins.

✓ Per-client and per-campaign card limits

✓ Auto-decline out-of-policy spend at point of purchase

✓ Real-time budget alerts before thresholds are hit

Turn big media buys into bigger returns. Earn 0.5% cashback on all card spend — including ad platforms, production, and media placements — and up to 50% back on business products.

Create separate budgets per client or project and track spend in real time. Eduvo notifies you when campaigns approach spending thresholds — before you go over, not after.

✓ Separate budgets per client, campaign, or channel

✓ Real-time spend tracking with automatic receipt capture

✓ Export client-billable expense reports at any time

Issue a virtual Visa card per vendor or freelancer with a hard spend cap. Invoices are captured automatically, approvals auto-routed — and every payment earns cashback.

"Eduvo has been a major gain for us in efficiency on T&E and client spend. It's easy for everyone to understand where and how to spend."

Daniel Cho

VP Finance, Cruxo Creative

Eduvo for Technology

Finance that fuels innovation.

Eduvo controls SaaS sprawl, gives every vendor its own virtual card, and offers cards with limits based on your business metrics — not a founder credit score.

Trusted by high-growth tech companies across Europe

Control spend and ship faster.

Fast-moving tech companies rely on Eduvo to remove financial friction so they can focus on building, scaling, and shipping.

Get cards with real-time controls.

Keep SaaS and cloud costs in check with vendor-level spend limits. Eduvo blocks out-of-policy spend at the point of purchase — with real-time alerts for policy violations before they hit the books.

✓ Per-vendor virtual cards with built-in limits

✓ SaaS subscription tracking — know every recurring charge

Give every contractor, cloud provider, and SaaS vendor its own virtual Visa card with a hard cap. Spend is captured and categorised automatically — and every charge earns cashback.

✓ Virtual cards per vendor with hard spend caps

✓ 0.5% cashback on all card spend — including cloud bills

Track expenses by tool, team, or project — with real-time receipt capture, intelligent policy enforcement, and automated approvals. Finance closes the books faster; engineering never loses momentum.

Tech companies spend heavily on software. Buy SaaS, tooling, and services through Eduvo partners and earn up to 50% cashback — on top of the 0.5% you earn on every card purchase.

✓ Up to 50% cashback on business products via Eduvo partners

✓ 0.5% cashback on all other card spend

✓ Cashback credited to your balance monthly — automatically

"Each month-end close gets better because Eduvo eliminated the last-minute scramble that used to slow us down."

Jonathan Smith

Lead Accounting Manager, Stackr

Eduvo for Consulting

Finance that goes wherever your consultants do.

Keep projects profitable from kickoff to client billing. Eduvo tracks spend by engagement, captures expenses in real time, and delivers client-ready reports without extra work.

Eduvo simplifies travel, card spend, and reporting to keep consultants focused on clients — not paperwork.

Stay profitable on every engagement.

Issue Eduvo Visa cards with client or engagement-level limits. Auto-enforce expense policies on every transaction and get real-time alerts before overspend cuts into project margins.

✓ Cards with per-engagement or per-client limits

✓ Separate budgets per project — visible in real time

Capture receipts instantly on mobile, apply per-diem policies automatically, and book flights and hotels directly in-platform. Consultants stay focused on delivery — not paperwork.

✓ Book flights & hotels directly in Eduvo — no reimbursements

✓ Auto-capture receipts on every card transaction

✓ Per-diem and travel policy auto-enforced at booking

Every transaction is captured with receipt, memo, and GL code the moment it happens, then synced to your accounting tool. Client-billable reports are ready in one click — no month-end scramble.

✓ GL coding and memos generated automatically

✓ One-click export of client-billable expense reports

Every card purchase on client work earns 0.5% cashback, and business products bought through Eduvo partners earn up to 50% back — margin recovered on every project.

✓ 0.5% cashback on all card spend

✓ Up to 50% cashback on business products via Eduvo partners

"Eduvo allows us to spend and bill across multiple European markets in local currency — which minimises our exposure to FX swings and keeps project margins clean."

Daniel Cho

Director, Finance Operations, Velofi Consulting

Help center

How can we help you?

Guides, FAQs, and documentation for everything in Eduvo.

Browse by topic

🚀

Getting started

Account setup, KYC, and your first card

💳

Cards & payments

Visa cards, limits, virtual cards, controls

💶

Cashback & rewards

0.5% on card spend, up to 50% on business products

📊

Expenses & receipts

Auto-capture, approvals, reporting

✈

Travel & cashback

Booking flights, hotels, cashback

🔒

Security & compliance

PCI-DSS, PSD2, GDPR, Visa Principal Member

Frequently asked questions

The answers our customers reach for most. Use the search above to filter.

How do I issue a virtual Visa card?

+

From your Eduvo dashboard, open Cards, choose New card, and select Virtual. Set the card name, spending limit, and any merchant controls, then create it — the card is ready to use instantly. Add it to Apple Pay or Google Pay, or copy the details for online payments. You can issue as many virtual cards as you need, including single-use cards for one-off purchases.

How fast can we get started?

+

Once your business has completed KYC/KYB verification — usually within minutes, all online — virtual Visa cards are ready to use immediately and physical cards arrive within days. There is no branch visit and no paperwork to post.

How do I set a spend limit on a card?

+

Open any card in the dashboard and edit its limit — you can set per-transaction, daily, or monthly caps. Limits change instantly and can be adjusted at any time. You can also lock a card to specific merchant categories, freeze it in one tap, or apply limits across a whole team rather than card by card.

How does Apple Pay work with Eduvo?

+

Every Eduvo Visa card — physical or virtual — can be added to Apple Pay and Google Pay. Open the card in the dashboard and tap Add to Apple Pay, or add it directly from your phone’s wallet app. Once added, you can pay in stores and online with your phone or watch, with the same limits and controls as the underlying card.

How do I submit a receipt?

+

You rarely have to chase it. When you pay with an Eduvo card, you get a push notification within seconds prompting you to snap a photo of the receipt. Tap once, take the photo, and it is matched to the transaction automatically. If a receipt is still missing, the system sends a reminder, so finance never has to chase it manually.

How do I book a flight in Eduvo?

+

Travel booking is built into the platform. Open Travel, search for flights or hotels, and book directly — the cost is charged straight to your company card, policy is enforced at the point of booking, and the expense is captured automatically. There is no separate travel tool and no reimbursement to process afterwards.

Is Eduvo regulated? Who safeguards funds?

+

Eduvo is a financial technology platform, not a bank. Banking and payment services are provided by our partner, a Payment Institution authorized by the Finantsinspektsioon (Estonian Financial Supervision and Resolution Authority) and an official Visa Principal Member (registration code 11812882), operating across the EEA and UK. Customer funds are safeguarded in segregated accounts under EMI safeguarding rules, kept separate from the institution’s own funds.

How much does Eduvo cost?

+

Eduvo offers Free, Pro, and Scale plans. The Free plan includes your first cards at no cost; paid plans add per-user features, travel booking, and the metal Visa Infinite card. No credit card is required to get started — see the Pricing page for current details.

How do I add my team to Eduvo?

+

Invite colleagues from the dashboard under Team, assign each a role — admin, manager, or member — and issue them a card with the limits and controls you choose. Role-based access means people only see what they need, and you can onboard your whole team in minutes.

Does Eduvo offer cashback?

+

Yes. Every card purchase earns 0.5% cashback, credited straight to your balance. Business products — software, SaaS, and services from Eduvo partners — earn up to 50% cashback. Cashback applies to all spend, including ad platforms and software subscriptions.

Which countries does Eduvo support?

+

Eduvo is currently live in Spain, the United Kingdom, Denmark, Sweden, and Norway, with more European markets coming soon. Businesses across the EEA and UK are supported.

How does Eduvo connect to my accounting software?

+

Eduvo exports clean, categorised transaction data to your accounting system, with GL codes set automatically through merchant-level rules. This keeps your books current without manual re-entry and turns month-end into a review rather than a data-entry sprint.

Is there a mobile app?

+

Yes. Eduvo is available on iOS and Android, with Apple Pay and Google Pay built in. You can issue cards, approve expenses, capture receipts, and freeze a card from your phone — wherever you are.

How do I freeze or cancel a card?

+

Open the card in the dashboard or mobile app and freeze it in one tap — useful if a card is lost or you spot something unusual. Freezing is instant and reversible; to cancel permanently, choose Cancel card. Virtual cards can be created and cancelled freely at any time.

No answers match your search. Try a different term, or contact our team.

Webinars

Level up your finance knowledge.

Join live sessions with Eduvo's product team, finance experts, and customers — or watch on-demand whenever it suits you.

🇳🇱 Amsterdam, Netherlands · Europe's biggest fintech event. Eduvo will be on the floor and hosting a breakfast roundtable for CFOs and finance leaders.

A milestone that reflects our speed, reliability, and user confidence.

Our Story

We started Eduvo with a simple idea: running business finances in Europe shouldn't mean juggling five different tools. We built the Brex for Europe — cards, expenses, and travel in one platform, on regulated Visa infrastructure that scales with you.

Our Mission

To give every European business access to world-class financial tools — from a two-person startup in Madrid to a 500-person scaleup in London. Powered by our partner's Visa infrastructure, regulated across the EEA and UK.

€2B+

Processed annually

5

Active markets: ES · UK · DK · SE · NO

Numbers

Numbers That Speak for Themselves

Trusted by businesses across Europe to move and manage money with confidence.

5,000+

Active businesses managing finances through Eduvo.

€2B+

Processed in European transactions every year.

5

Markets: Spain, UK, Denmark, Sweden, Norway.

10

EUR, USD, GBP, SEK, NOK, DKK, PLN, CZK, HUF, RON

5,000+

Active businesses managing finances through Eduvo.

Issue physical and virtual Visa cards to your team in seconds. Set per-card limits, lock categories, and track every transaction in real time.

Earn Cashback

0.5% cashback on all card spend, and up to 50% back on business products — software, SaaS, and services through Eduvo partners

Automate Expenses

Capture receipts automatically, route multi-step approvals, and close the books faster. 99% policy compliance, zero manual chasing.

Travel Booking & Cashback

Book flights and hotels directly in the platform. Every purchase earns 0.5% cashback — and up to 50% on business products. Scale plan adds metal Visa Infinite cards with worldwide lounge access.

"We're redefining how European businesses connect with their money — making finance feel simple, fast, and built for how modern teams actually work."

Jordan PatelHead of Design, Eduvo

Our Team

The people behind Eduvo

Fintech builders, ex-bankers, and product people united by the belief that European businesses deserve better financial tools.

Alex Warren

Founder & CEO — Turning complex financial tools into simple, empowering experiences.

Maya Chen

CTO — Building reliable infrastructure that scales across every European market.

Jordan Patel

Head of Design — Designing experiences that make business finance feel human.

Get started

Take control of your business finances today

Power Your Finances

Manage spend, automate workflows, and boost efficiency with Eduvo's complete financial platform for European businesses.

Discover the core tools that make managing your business finances faster, smarter, and more transparent.

Visa Corporate Cards

Issue physical, virtual, and metal Visa cards instantly. Set per-card spend limits, freeze in one tap, enable Apple Pay and Google Pay. Scale plan includes a premium metal Visa Infinite card with worldwide airport lounge access.

Business Travel & Cashback

Book flights and hotels directly in Eduvo at market rates. Every booking is charged to your company card, earns cashback, and lands in your expense reports automatically — no reimbursements, no lost receipts. Plus 0.5% cashback on all card spend and up to 50% on business products via Eduvo partners.

Expense Management

Automated receipt capture, multi-step approval workflows, and real-time reporting. Employees submit expenses in seconds; finance teams approve and close the books faster — with 99% policy compliance.

Move money

Move money. Grow faster.

Introducing Eduvo — the complete financial platform for European businesses. Powerful, seamless way to manage cards, expenses, and travel — all from one place.

Get started in just a few simple steps — Eduvo makes finance effortless from setup to growth.

01

Create Your Account

Sign up and complete KYC in minutes. No complex setup, no branch visits required.

02

Issue Your Cards

Issue physical and virtual Visa cards to your team — ready to spend in minutes.

03

Configure Your Setup

Set spend policies, approval workflows, and team permissions to match your business.

04

Get Support Anytime

Access our help centre or chat with our support team 24/7 — in your language.

Take Control With Every Transaction

Our Clients

Trusted by Businesses That Move Money Forward

FinWave

A next-gen fintech startup using Eduvo to automate card spend and reconcile expenses in real time — saving hours every week on financial operations.

HealthSync

A health tech platform that uses Eduvo to manage pan-European card spend and expense reporting across 4 markets, replacing a patchwork of disconnected tools.

EduSphere

An edtech scaleup using Eduvo's virtual cards and travel booking to manage conference trips and team spend across Spain, UK, and Sweden from one dashboard.

GreenNest

A sustainable home tech company running all procurement and team expenses through Eduvo, with automated approval flows that replaced a 3-week manual process.

TravelVerse

A travel startup that books all client trips through Eduvo's built-in travel feature, charging directly to company cards — zero reimbursements, full visibility.

Cash flow

Simplified cash flow, easy control.

From card spend to cash flow — all from one powerful platform. Spend smarter, gain more control, and keep your business moving.

3x YoY growth

Average revenue growth for Eduvo customers in year 1

Connect your favorite tools and platforms effortlessly. From cards to accounting, Eduvo keeps your business running smoothly across Europe.

Visa & Card Networks

ERP & HR Systems

Accounting Tools

Travel & Booking APIs

Consistent Growth

€10M+

Annual volume processed — and growing 3x YoY

"Our mission is simple — make finance effortless so European businesses can focus on what truly matters."

Jordan PatelHead of Design, Eduvo

3x YoY growth · Trusted by 5,000+ businesses

Book a demo

See Eduvo in action.

We'll walk you through the platform in 30 minutes — cards, expenses, travel, and cashback. No sales pressure, just a real look at how it works for businesses like yours.

30-minute live walkthrough

A product specialist shows you the platform end-to-end, live — no pre-recorded slides.

Tailored to your business

Tell us your team size and markets — we'll focus on what's most relevant to you.

No commitment required

A demo is just a demo. We'll answer your questions and let the product do the talking.

Response within 1 business day

Submit the form and we'll reach out to confirm a time that works for you.

Request your demo

Fill in your details and we'll be in touch within 1 business day.

You're booked in.

We'll reach out within 1 business day to confirm a time. Check your inbox — and your spam folder, just in case.

Annual billing: 2 months free · All prices exclude VAT

Included in Grow & Scale

AI CFO — the intelligence layer everything feeds.

Ask questions in plain language. Get instant answers about burn rate, runway, team spend, and vendor costs — all live.

✓ Live burn rate & runway prediction

✓ Automatic vendor audit & duplicate detection

✓ One-click board pack monthly

✓ Natural-language spend queries

Live examples

YOU

At current burn, what’s our runway?

EDUVO AI

11.3 months remaining

YOU

Which team is over budget?

EDUVO AI

Engineering — 23% over

Compare features

Feature

Starter

Grow

Scale

Cards

Virtual Visa card

1

Unlimited

Unlimited

Physical Visa card

—

✓

✓

Metal Visa Infinite

—

—

✓

Cashback

—

0.3%

0.5%

Expenses & spend

Basic transaction history

✓

✓

✓

Full expense management

—

✓

✓

Approval workflows

—

✓

✓

Policy-as-code controls

—

—

✓

Accounting integrations

—

✓

✓

Travel

Travel booking

✓

✓

✓

Travel & purchase insurance

—

—

✓

Airport lounge access

—

—

✓

AI CFO

Burn rate & runway

—

✓

✓

Natural-language queries

—

✓

✓

Automated board pack

—

✓

✓

Support

Email & chat support

✓

✓

✓

Dedicated account manager

—

—

✓

FAQ

Frequently asked questions

Everything you need to know about Eduvo pricing.

Is the Starter plan really free?

+

Yes. Starter is free for 1 user with no time limit. You get 1 virtual Visa card, travel booking access, and cashback on your card spend. You only pay when you add more users or upgrade.

How does annual billing work?

+

Annual billing gives you 2 months free (equivalent to about 17% off). You pay for 12 months upfront at the discounted rate.

Can I add users at any time?

+

Yes. On Grow and Scale, each additional user is billed at the per-user rate. You can add or remove users at any time and billing adjusts from your next statement.

What is the AI CFO?

+

The AI CFO is a natural-language intelligence layer across all six pillars. Ask questions like “What’s our runway?” or “Which team is over budget?” and get instant answers from your live transaction data. It also generates automated board packs monthly.

Can I upgrade or downgrade between plans?

+

Yes. Upgrades take effect immediately. Downgrades take effect at the end of your current billing cycle.

.svg)

.svg)

.svg)